A Systematic Withdrawal Plan (SWP) allows investors to withdraw a fixed amount from their mutual fund investment at regular intervals (monthly/quarterly). It helps generate a steady income while the remaining investment continues to stay invested and grow over time.

A Systematic Withdrawal Plan (SWP) is an ideal solution for investors who want to generate regular income from their mutual fund investments while keeping the remaining amount invested for long-term growth.

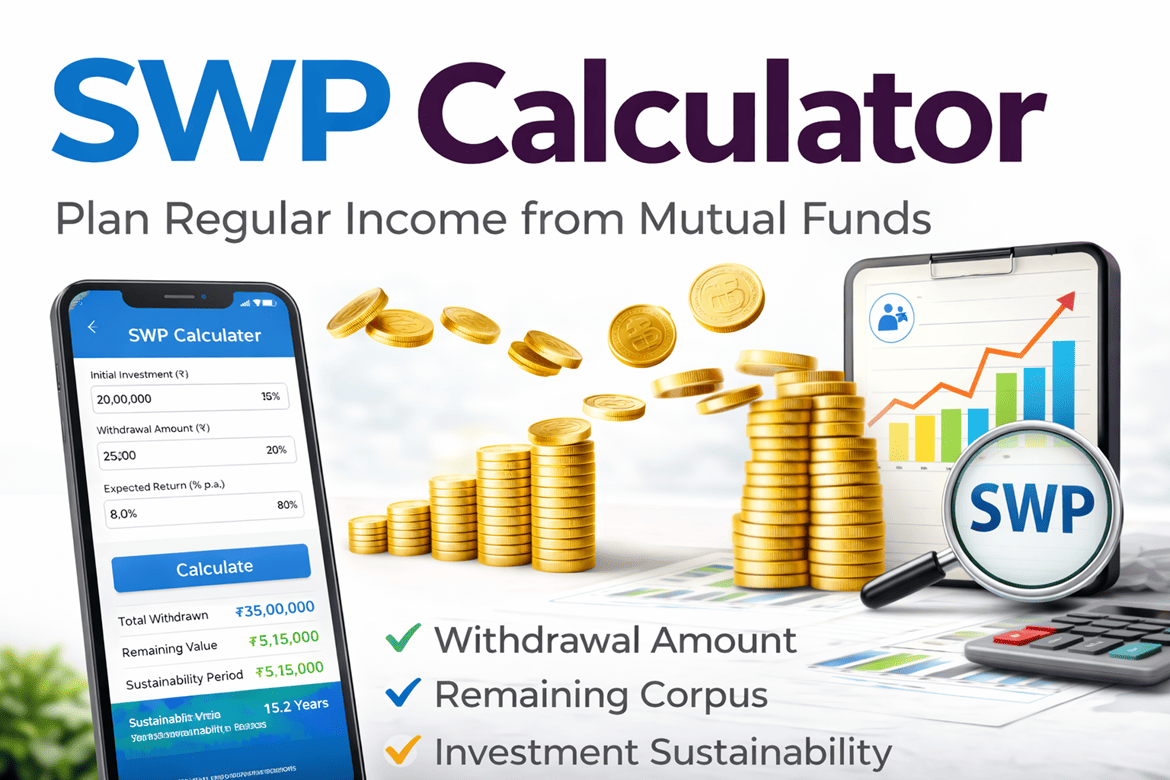

Our SWP Calculator helps you estimate how long your investment will last and how much income you can withdraw periodically—monthly, quarterly, or annually.

An SWP allows investors to withdraw a fixed amount at regular intervals from their mutual fund investment. It is commonly used by retirees, senior citizens, and individuals seeking stable cash flow without redeeming the entire investment at once.

✅ Regular income generation

✅ Tax-efficient withdrawals

✅ Capital remains invested

✅ Flexible withdrawal amount & frequency

✅ Ideal for retirement planning

The SWP calculator estimates the remaining investment value after regular withdrawals, considering the expected rate of return.

Initial investment amount

Withdrawal amount

Expected annual return (%)

Withdrawal frequency

Investment duration

Total withdrawn amount

Remaining investment value

Investment sustainability period

📌 Note: Actual returns may vary depending on market performance.

The calculator considers:

Compounded growth on remaining balance

Periodic withdrawals

Market-linked return assumptions

This helps you understand how long your corpus can support withdrawals.

An SWP calculator helps you:

✔ Plan post-retirement income

✔ Avoid premature exhaustion of capital

✔ Compare different withdrawal scenarios

✔ Optimize withdrawal amount

It ensures you withdraw smartly without harming long-term wealth.

| Investment | Monthly SWP | Expected Return | Duration |

|---|---|---|---|

| ₹50,00,000 | ₹25,000 | 8% | 20+ years |

| ₹30,00,000 | ₹20,000 | 7% | 15+ years |

(Approximate values for illustration)

SWP is ideal for:

Retired individuals

Senior citizens

Investors seeking passive income

People shifting from growth to income phase

Anyone avoiding lump-sum redemption

SWP returns are market-linked

Higher withdrawal = faster capital erosion

Long-term investment helps sustain SWP

Equity SWP has higher risk than debt SWP

SWP can be more tax-efficient and flexible than FDs, especially for long-term investors.

Yes. Tax depends on capital gains rules of equity or debt mutual funds.

Yes, SWPs are flexible and can be modified or stopped anytime.

Debt funds, hybrid funds, and conservative equity funds are commonly used.

At GMD ThriveX, we help you:

Choose the right SWP strategy

Balance income & capital protection

Optimize tax efficiency

Build sustainable retirement income