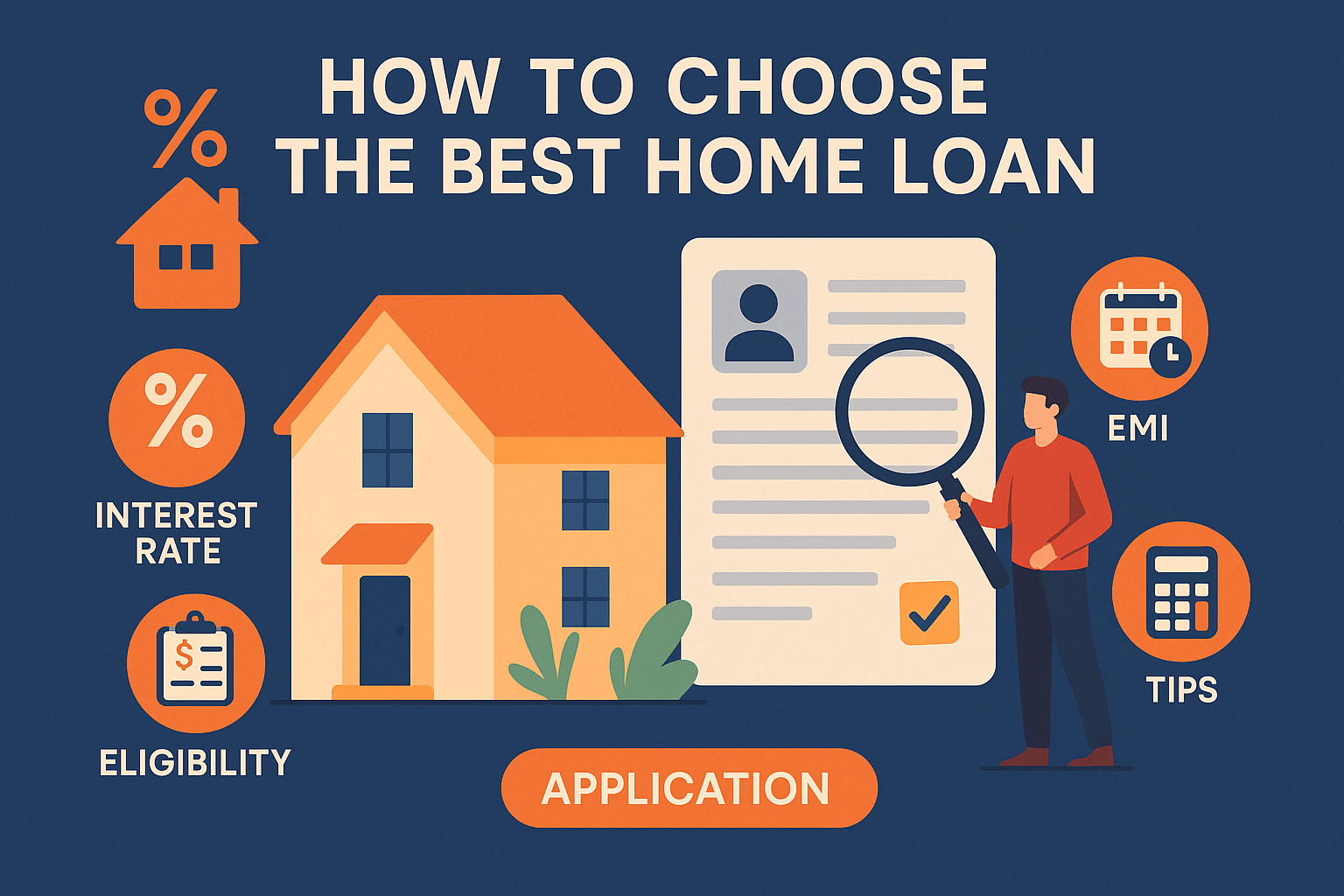

Buying a home is one of the biggest financial decisions in life. A good home loan can save you lakhs over time — while a wrong one can create long-term financial stress. That’s why choosing the best home loan is extremely important.

This complete guide explains how to choose the right bank, rate, tenure, documents, and how to reduce EMI burden smartly.

✔ A. Regular Home Loan

For buying a ready-to-move or under-construction property.

✔ B. Home Construction Loan

For constructing your own house on a plot.

✔ C. Home Renovation Loan

For repairs, upgrades, and remodeling.

✔ D. Plot Purchase Loan

For buying a residential plot of land.

✔ E. Balance Transfer Loan

Transfer your home loan to another bank at a lower interest rate and SAVE huge interest.

Interest rate decides your total cost of the loan.

📌 Types of Interest Rates

Floating Rate → Most preferred, reduces when RBI cuts rates

Fixed Rate → EMI stays the same, even if rates increase or decrease

📉 Current Interest Rate Range (2025)

Most banks/NBFCs offer rates between 8.25% – 10.50% depending on:

CIBIL Score

Loan amount

Income stability

Property type

Tip: Even a 0.50% lower rate can save you lakhs over 20 years.

Banks consider:

✔ Income & job stability

Higher income = higher loan approval.

✔ Age

Younger buyers get longer tenures.

✔ CIBIL Score

A score above 750 ensures lower interest rates.

✔ Existing Loans

Too many EMIs reduce eligibility.

✔ Co-applicant (optional)

Adding spouse increases loan approval and amount.

📌 Basic documents:

PAN & Aadhaar

Latest photographs

Bank statements (6–12 months)

Income proof (salary slips/ITR)

Address proof

📌 Property documents:

Agreement to sale

Builder NOC

Title deed

Approved plan

Tip: Keep documents ready to get faster approval.

✔ Short Tenure = Higher EMI but LOW interest

✔ Long Tenure = Lower EMI but HIGH interest

Most home buyers choose 20–25 years tenure.

Recommendation: Keep a longer tenure but prepay aggressively to save interest.

If your current bank is charging high rates:

👉 Transfer to another bank offering a lower rate

👉 Save ₹2–5 lakhs (or more) easily

👉 Works best in first 5–8 years

Always compare processing fees before switching.

Processing fee

Legal & technical charges

Insurance bundling

Foreclosure charges (for fixed-rate loans)

Choose a transparent lender.

⭐ Improve your CIBIL score

⭐ Add a co-applicant

⭐ Compare lenders before finalizing

⭐ Avoid too many loan applications

⭐ Try to pay 20–30% down payment

⭐ Prepay whenever you get surplus income

1. How much home loan can I get?

Usually 40–60% of your monthly income.

2. Should I choose fixed or floating rate?

Floating is better for long-term loans.

3. Can I repay the home loan early?

Yes. Floating-rate home loans have zero prepayment charges.

4. What is the ideal credit score for home loan approval?

A score above 750 gives best interest rates.

Confused about which bank offers the best home loan?

At GMD ThriveX, we help you compare interest rates, choose the best lender, maximize loan eligibility, and reduce EMIs smartly.

📞 Contact us to get your free home loan consultation.